Why we backed Runo

Runo is the kind of company that the conventional VC model misses entirely. It is profitable. It is unsexy. It serves Indian MSMEs whose CIO no one has ever heard of. And it is one of the highest-return-per-dollar SaaS businesses in our portfolio.

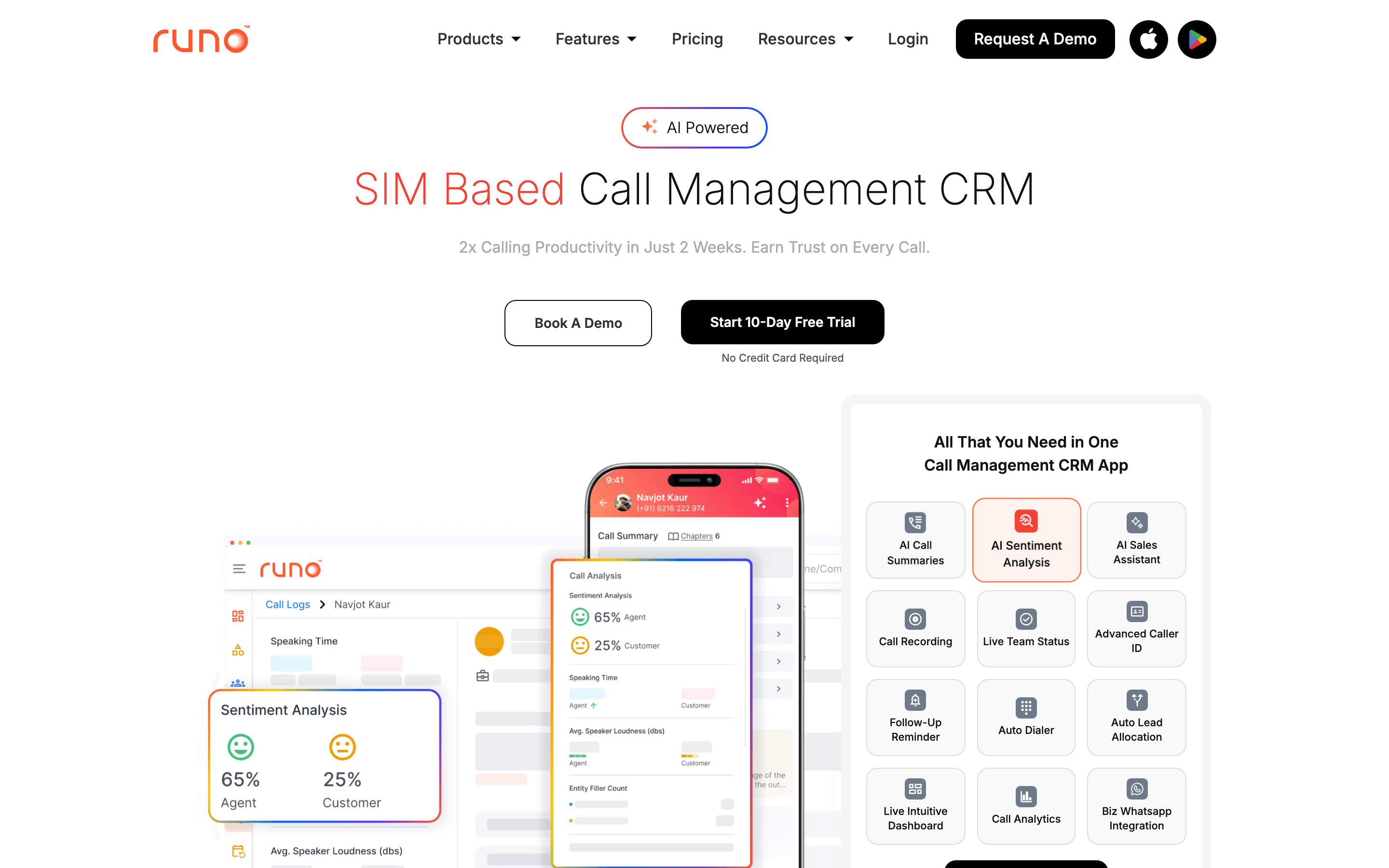

SIM-based mobile call CRM for outbound sales teams.

The company

Runo is a SIM-based mobile call-management CRM. In plain English: it gives every outbound salesperson a dedicated business SIM, then tracks every call they make at the SIM level — outbound, inbound, recorded, with real-time analytics on call volume, agent productivity, and lead conversion. It sits inside a mobile-first CRM that those same salespeople use to log notes, manage pipeline, and report to their managers.

Runo currently serves over 450 paying customers and 7,000+ licenses, with annual recurring revenue around $750K and a strong path to $1M ARR. Most of those customers are Indian MSMEs in insurance, lending, real estate, edtech, automotive, and recruitment — outbound-sales-heavy verticals where the difference between a controlled, measurable sales floor and a chaotic one is the difference between profitability and zero. Enterprise wins include Honda, Hyundai, and Bajaj Finserv.

Why we backed them

The first time we saw Runo, the obvious question was: doesn't cloud telephony already do this? The answer turns out to be no — at least, not for the customer Runo serves.

Cloud telephony was built for call-center environments where every agent sits at a desk, takes a wired headset, and works inside a fixed software stack. Indian outbound sales reality is different. Salespeople are mobile. They move between cities. They take calls in a customer's office, in a parking lot, on a tier-2 highway. They use their personal mobile or a company SIM, not a softphone. For that workforce — which is ten million-plus people in India alone — cloud telephony is the wrong primitive.

Runo built the right primitive. It treats the SIM as the unit of measurement, the mobile phone as the workstation, and the salesperson's everyday behavior as the input. Every call, every contact, every voice note flows automatically into a CRM that the manager can see in real time, without changing the salesperson's daily workflow.

Three reasons we backed them.

First, the unit economics are exceptional. Runo's customer is paying a per-license SaaS fee that replaces a more expensive cloud-telephony contract while delivering more useful data. The brand-new customer recovers their first-year investment in months, not quarters. The churn is real — about 5% monthly, mostly bandwidth-driven on the customer-success side — but the LTV/CAC math is robust.

Second, the moat compounds with scale. Every additional customer makes the underlying mobile-network integration deeper, the carrier relationships more entrenched, and the AI-driven call-analytics engine more accurate. Competitors entering today are starting with a structural data deficit.

Third, the founders run an actual business. Runo is in many ways the anti-VC company — they are profitable, capital-efficient, and they prioritize customer retention over growth-at-all-costs. That is exactly the founder profile we want to back.

What we did beyond capital

We worked with the Runo team on the transition from MSME-led growth to enterprise-grade growth. The Honda and Bajaj Finserv wins demonstrated that Runo's product can clear enterprise security and procurement bars; the question was how to scale the motion.

We made introductions to enterprise sales operations leaders in our network — heads of sales at NBFCs, edtech companies, and real estate platforms that fit Runo's enterprise ICP. Several of those conversations became contracts.

We supported the team on AI integration positioning. Runo's roadmap includes embedded AI features for call summarization, lead scoring, and coaching; we helped frame that capability against the mobile-CRM competitive set in a way that moves Runo up-market.

The Callapina conviction

Vertical SaaS for India's underserved MSME segment is one of the structurally most attractive corners of the early-stage venture market. The companies are unfashionable, the operators are pragmatic, the unit economics are sound, and the addressable market is enormous. Runo is one of the strongest expressions of that thesis we have seen.

— Vinod Jose, Founding GP

More portfolio case studies

Why we backed Orca AI

B2B customer teams are drowning in disconnected account signals — support tickets, success notes, product usage, sales context, and renewal risk. Orca AI is the layer that turns those signals into a customer-decision substrate.

Why we backed Skydda

On April 7, 2026, an AI model read the Linux kernel and found vulnerabilities thousands of human engineers had missed for decades. The defender's edge in the world that announcement created is no longer about scanning faster — it is about knowing your specific business deeply enough to detect a patient, business-aware attacker.

Why we backed Bynry

There are over one hundred thousand small and mid-sized water, electric, and gas utilities in North America, and almost every one of them is running customer-information software that was written before the iPhone was invented. Bynry is the AI-native platform that finally makes their modernization economically viable.

See the company overview, traction signals, founder perspective, and related diligence context.