Investing in Innovation: should you go direct, or trust the fund?

The decision to invest in startups should not be taken in isolation; it should be in relation to the rest of your portfolio. Direct vs. fund is a question of expertise, time, and conviction — not just returns.

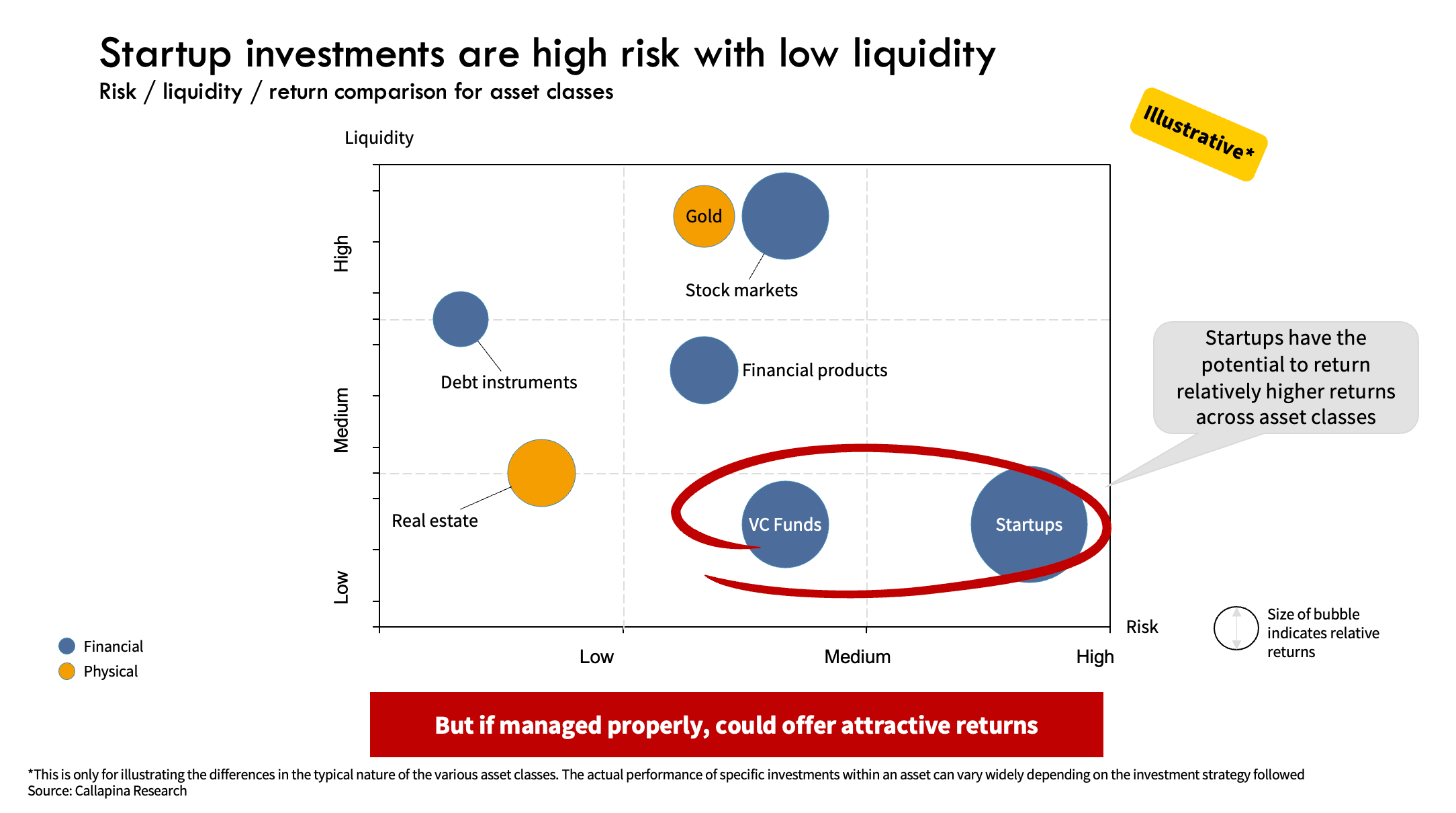

Investing in startups versus other asset classes

Investing in the world of startups offers the allure of high returns and the excitement of nurturing the next big innovation. But the decision to invest in startups should not be taken in isolation; it should be in relation with the rest of your portfolio, and you should be clear on the role that startups as an asset class fulfill in your overall investment strategy.

As an investor, you have two primary avenues to participate in this space: directly investing in individual startups, or investing in a venture capital (VC) fund. Each path has its own set of advantages, risks, and considerations.

Direct startup investment

Direct startup investment involves personally providing capital to a startup company in exchange for equity ownership. This method allows you to select specific startups, giving you control over where your money goes.

Pros: potential for very high returns; direct involvement and control; personal satisfaction from contributing to industries you care about.

Cons: high risk of total loss; lack of diversification; long illiquidity; significant time and resource commitment for sourcing, diligence, and mentoring.

What to look for: a strong founding team, a scalable business model, a real market opportunity, and the discipline to do thorough due diligence on financials, legal standing, and competitive landscape.

Venture capital fund investment

A VC fund pools capital from multiple investors to invest in a diversified portfolio of startups, managed by professional fund managers. As a limited partner, you own a share of the fund proportional to your investment.

Pros: professional management; diversification across a portfolio; access to deal flow that would be hard to source individually; reduced time commitment.

Cons: management fees and carried interest reduce net returns; limited control over investment selection; high minimum commitments.

What to look for: experienced fund managers with a documented track record, a clear and defensible investment thesis, a fee structure you understand, and a strategy that aligns with your goals.

A side-by-side view

| Criterion | Direct startup investment | VC fund investment |

|---|---|---|

| Control | High | Low — fund managers decide |

| Diversification | Limited unless you can write many checks | Broad — built into the structure |

| Expertise required | High (industry + diligence) | Lower (rely on the GP) |

| Time commitment | Significant | Minimal |

| Liquidity | Low (5-10y) | Low (7-10y) |

| Minimum check | Flexible | Substantial |

| Fees | Transaction fees | Management fee + carry |

A hybrid approach

Many experienced investors choose a hybrid: directly investing in select startups while also participating in VC funds. This combines personal involvement on a few high-conviction deals with the diversification and professional management of a fund.

The right answer depends on your financial goals, risk appetite, expertise, and the level of involvement you want. Direct investment offers the thrill of hands-on participation and the potential for outsized returns, but it demands time, expertise, and tolerance for concentrated risk. Venture funds provide a more passive position with professional management, but require trust in the fund managers and acceptance of fees.

The point isn't to pick one and dismiss the other. It's to be clear-eyed about which role each plays in your portfolio.

— Vinod Jose, Founding GP

Suggested articles

How we exited Aisle — anatomy of a deal

Info Edge — parent of Naukri, 99acres, and Jeevansathi — bought 76% of Aisle in March 2022 for ₹91 crore, then walked the stake to 100% over the next three years. The deal validated a thesis that Indian consumer-internet incumbents would pay strategic prices for high-intent vertical brands. And it brought us back the founder twice — once at exit, then again as the founder of Jamm in our Fund I portfolio.

How we exited Carestack — anatomy of a deal

Carestack is the headline win on the Callapina angel ledger — eight-year hold, Accel-led Series A brought in by us, $145M+ subsequently raised, full exit. The deal is the cleanest illustration of the four-pillar thesis working in practice: an Indian-data-native vertical, a North-America go-to-market, and an operator-led founder backed before consensus formed.

Why we backed Casa Melhor

Casa Melhor is building the infrastructure layer for enterprise accommodation — dedicated, tech-enabled Business Residences that replace fragmented hotel stays for companies with recurring employee travel.

See the rest of our portfolio, the four-pillar thesis behind every bet, and our public track record.